December 12, 2012

Distillers Grains and Solubles: Its Role in the Livestock Industries

With the rapid expansion of US corn starch ethanol production since the mid-2000s, its major co-product, Distillers Grain and Solubles (DGS) supplies also have increased sharply every year from the 2005-06 through 2010-11 September-August marketing years. DGS is the major product remaining after the starch in corn has been processed into ethanol. It is a medium-protein feed ingredient and also contains substantial feed energy. DGS can be fed wet, partially dried, or dried to 10% moisture. In some cases, corn oil is partially removed from DGS to be used for biodiesel production or to be returned to the feed industry as a separate ingredient. In other situations, syrup remaining after ethanol production is used as a cattle feed along with roughages to replace corn. About 28 to 30% of the original weight of corn is left as DGS (at 10% moisture) after ethanol production. The amount varies slightly depending on the ethanol yield of the plant and whether corn oil is removed. This feed ingredient thus has an important role in replacing both corn and soybean meal in livestock and poultry rations. The US livestock and feed industries have learned that it can be used in rations at much higher levels than were believed feasible a few years ago.

In this article, we review trends in DGS production, uses, and price relationships to corn and soybean meal as well as an emerging issue. With reduced ethanol production that is occurring this marketing year, DGS supplies have tightened and most likely will continue to be tighter than in the recent past until the 2013 US corn crop is harvested.

Trend in Production Figure 1 shows US corn processing for ethanol and DGS production since the 2004-05 marketing year. This year we expect US production of DGS to decline by about 10% from the September 2011-August 2012 marketing year because of the severe US drought and resulting very tight US and global corn supplies. The actual amount of decline in production is still somewhat uncertain. It will depend on the final size of the US corn crop, which in early January could be revised modestly from USDA's November crop report. DGS production also will depend on whether or not there is a change in the mandated volume of corn-starch ethanol to be blended in US gasoline supplies, the amount of ethanol from Brazil that can be imported into the US this season, and the prices of both ethanol and gasoline. Even without a reduction in the government-mandated volume of ethanol to be used in gasoline, the US ethanol industry has some flexibility to reduce its production by using excess RINs or renewable identification numbers. These are identification numbers assigned to each gallon of ethanol when it is produced. They are used to enforce the mandated amount of corn-starch ethanol to be blended with gasoline each year. For the last 5 years, the ethanol industry has produced more ethanol than mandated. That has allowed ethanol blenders to build up credits with these RINs that can be substituted for actual blending when corn supplies are tight.

Trend in Production Figure 1 shows US corn processing for ethanol and DGS production since the 2004-05 marketing year. This year we expect US production of DGS to decline by about 10% from the September 2011-August 2012 marketing year because of the severe US drought and resulting very tight US and global corn supplies. The actual amount of decline in production is still somewhat uncertain. It will depend on the final size of the US corn crop, which in early January could be revised modestly from USDA's November crop report. DGS production also will depend on whether or not there is a change in the mandated volume of corn-starch ethanol to be blended in US gasoline supplies, the amount of ethanol from Brazil that can be imported into the US this season, and the prices of both ethanol and gasoline. Even without a reduction in the government-mandated volume of ethanol to be used in gasoline, the US ethanol industry has some flexibility to reduce its production by using excess RINs or renewable identification numbers. These are identification numbers assigned to each gallon of ethanol when it is produced. They are used to enforce the mandated amount of corn-starch ethanol to be blended with gasoline each year. For the last 5 years, the ethanol industry has produced more ethanol than mandated. That has allowed ethanol blenders to build up credits with these RINs that can be substituted for actual blending when corn supplies are tight.

This year's decline in DGS production will likely be temporary. For the longer term, the US motor fuel industry and motorists will probably accept E-15, which is a blend of 15% ethanol and 85% gasoline. The US Environmental Protection Agency (EPA) has approved its use for conventional cars and light trucks produced since 2001, but time will be needed for retail fuel stations to develop the infrastructure for marketing it. If it is widely accepted, it could increase US ethanol production by one-third or more in future years. A significant part of that increase probably will come from increased production of ethanol from corn starch, although some fraction may also come from cellulosic ethanol.

Figure 2 shows weekly US fuel ethanol production since September 1, 2010 and the average weekly production needed to meet USDA's 4.5 billion bushels of corn processed for ethanol and DGS in the current marketing year. The weekly average from September 1 through November 2 was marginally higher than needed to meet the projection, although weekly production during the last week of October and the first week of November converted to an annual rate exceeded the USDA projection by about 70 million bushels corn equivalent. If this rate were to continue for the rest of the marketing year, DGS supplies would be slightly larger than currently projected.

Figure 2 shows weekly US fuel ethanol production since September 1, 2010 and the average weekly production needed to meet USDA's 4.5 billion bushels of corn processed for ethanol and DGS in the current marketing year. The weekly average from September 1 through November 2 was marginally higher than needed to meet the projection, although weekly production during the last week of October and the first week of November converted to an annual rate exceeded the USDA projection by about 70 million bushels corn equivalent. If this rate were to continue for the rest of the marketing year, DGS supplies would be slightly larger than currently projected.

Figure 3 shows our estimates of the amount of the amount of DGS fed by species in the US and exported. DGS is very well-suited for cattle and other ruminants. When fed to beef cattle, a pound of DGS can replace more than a pound of corn. For other species, the corn replacement ratio tends to be somewhat lower but DGS also replaces soybean meal or other protein feed ingredients. Because of differences in digestive systems of swine and poultry vs. ruminants, DGS feeding rates are lower but still significant with these species than for cattle. Thus, the largest domestic users of DGS are the beef and dairy industries. DGS exports have expanded substantially in the last few years and likely will increase further in the next several years if the amount of corn processed for ethanol can be increased.

Figure 3 shows our estimates of the amount of the amount of DGS fed by species in the US and exported. DGS is very well-suited for cattle and other ruminants. When fed to beef cattle, a pound of DGS can replace more than a pound of corn. For other species, the corn replacement ratio tends to be somewhat lower but DGS also replaces soybean meal or other protein feed ingredients. Because of differences in digestive systems of swine and poultry vs. ruminants, DGS feeding rates are lower but still significant with these species than for cattle. Thus, the largest domestic users of DGS are the beef and dairy industries. DGS exports have expanded substantially in the last few years and likely will increase further in the next several years if the amount of corn processed for ethanol can be increased.

Figure 4 shows the explosive growth of US DGS and closely related product exports by country of destination in the last few years. Major export markets for these products have included Mexico and Canada, and more recently a large number of other countries. In the 2009-10 marketing year, China became a large importer of US DGS.

Figure 4 shows the explosive growth of US DGS and closely related product exports by country of destination in the last few years. Major export markets for these products have included Mexico and Canada, and more recently a large number of other countries. In the 2009-10 marketing year, China became a large importer of US DGS. It accounted for about one-fourth of that year's US DGS exports. In the next year, China began an investigation to determine whether the US was unfairly subsidising DGS exports and its DGS imports declined slightly. However, the Chinese government halted its investigation in about mid-2012, perhaps partly as a result of the expiration of the US ethanol blenders' tax credit. Since then, interest of its feed industry in importing DGS has been strong. The Chinese government is now implementing new policies that require approval of individual plants for shipments of DGS to its markets. At this writing, it is uncertain what implications this may have for US DGS exports to China. China has a substantial fuel ethanol industry that also produces DGS and its ethanol producers are sensitive to imports from the US. For the longer term, there appears to be a large potential market there for both US and Chinese DGS supplies.

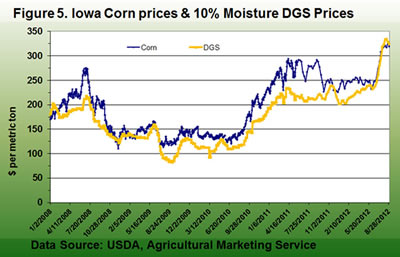

Figures 5 and 6 show DGS prices as percentages of corn and soybean meal prices through early September of this year. For several years, DGS prices per pound or per tonne had tended to be moderately below corn, except for limited seasonally strong demand periods during the winter.

Figures 5 and 6 show DGS prices as percentages of corn and soybean meal prices through early September of this year. For several years, DGS prices per pound or per tonne had tended to be moderately below corn, except for limited seasonally strong demand periods during the winter.

However, with the onset of this year's severely reduced corn and soybean production, DGS prices have moved closer than normal to corn prices and at times this fall have exceeded corn prices. The change in the price relationship reflects tight supplies of both corn and soybean meal. Record or near-record high soybean meal prices likely have allowed DGS prices at times to exceed corn prices as the market more closely reflected their protein value.

As shown in Figure 6, DGS prices have followed the strong upward trend in soybean meal prices this year as the soybean meal market responded to very adverse weather in South America that reduced yields on its soybean crop harvested in the early months of this year and the severe US drought that reduced US production.

As shown in Figure 6, DGS prices have followed the strong upward trend in soybean meal prices this year as the soybean meal market responded to very adverse weather in South America that reduced yields on its soybean crop harvested in the early months of this year and the severe US drought that reduced US production.

The final size of foreign feed crops, especially those in South America, Russia, Kazakhstan, and Ukraine, as well as the amount of feed wheat available from Australia will be influencers on the prices of DGS in the months ahead, along with final US crop estimates for the 2012 growing season. The latter estimates will be released in early January, along with revised USDA estimates of 2012 foreign crop production and updated projections of the expected South American crops. Current indications are that global feed grain supplies will be very tight for most of this marketing year and that feed wheat supplies will become tighter in the months ahead. South American corn supplies appear almost certain to tighten significantly in the next several months and foreign buyers of US corn appear to have limited forward coverage. These conditions indicate there is a significant potential for tightening global feed supplies in the next several months. If so, that will affect the cost and availability of DGS for the US domestic livestock and poultry industries. Soybean and soybean meal supplies also will be very tight for the next few months, but may be somewhat more plentiful from March 2013 onward if South America has normal weather in the next several months. Because of reduced supplies all feed ingredients, DGS prices will continue to be significantly higher than last season. DGS prices will be influenced by both the price of corn and the price of soybean meal. They likely will continue to be competitive with both of those ingredients but not quite as competitive as in past years.