April 19, 2023

A general perspective of Chinese feed enterprises

The scale and integration of China's animal husbandry pushed the development of Chinese feed enterprises with an output of more than one million tonnes.

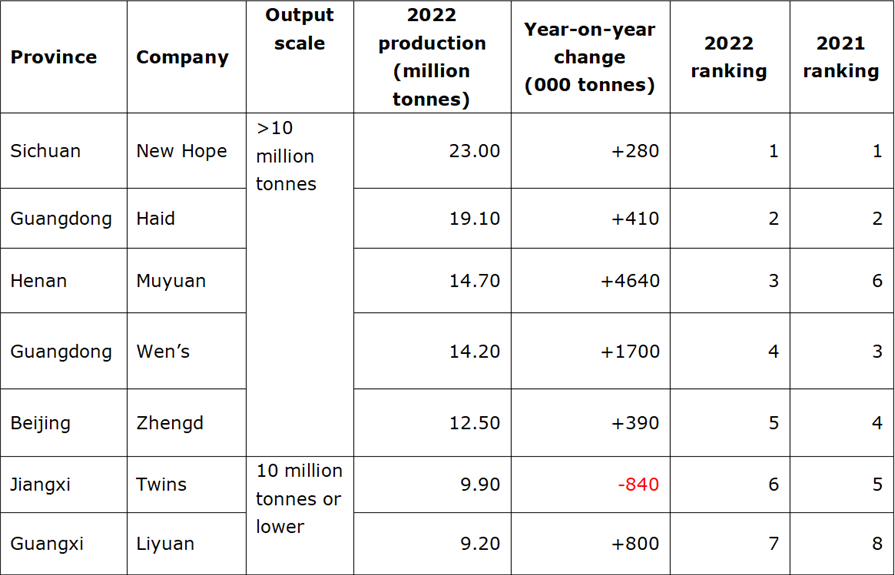

Last year, there are 37 feed groups with an output exceeding one million tonnes. The combined feed output of these companies reached 183 million tonnes, an increase of 3.39% over 2021.

Furthermore, there are five mega-sized groups with an annual output of more than 10 million tonnes in the past two years.

Sichuan New Hope is China's largest feed group. Its output of pig feed is nearly nine million tonnes. The company made efforts to develop aquatic feed through the acquisition of aquatic feed factories in the past two years. Its feed production reached 1.2 million tonnes in 2022.

Guangdong Haid Group, the second largest Chinese feed production group, is among those with a production capacity of more than 10 million tonnes. Almost all its feed is exported. Haid's output of hog feed increased from 4.8 million tonnes in 2021 to 5.30 million tonnes in 2022. Its production of layer poultry feed also increased from 2.90 million tonnes in 2021 to 3.20 million tonnes in 2022.

Henan Muyuan is a single enterprise that integrates pig breeding. It will be the only company with an output of pig feed exceeding 10 million tonnes.

Guangdong Wen's is the largest pig and broiler chicken breeding contract enterprise in China. Originally the largest pig farming enterprise in the country, it overcame the impact of African swine fever and rose steadily in the last two years.

Chia Tai Group, the largest foreign-funded feed enterprise in China, focuses on the integration of laying hens and pigs as part of its development. Concerning the integration of laying hens, Chia Tai has a scale of 17 million.

The feed output of the aforementioned groups has been stable at more than 10 million tonnes for several years.

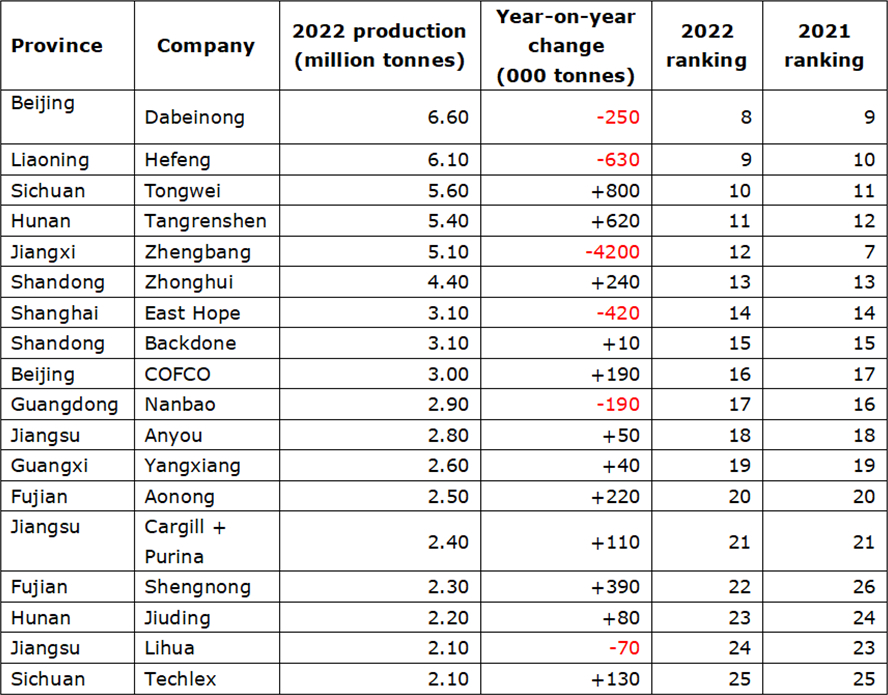

In China, there are 18 feed groups with outputs of 5-10 million tonnes. Among these groups, Jiangxi Zhengbang saw the biggest change in yearly ranking. However, it also recorded the biggest decline in feed production. In another development, following the disclosure of the 2022 annual report of Zhengbang Technology, the Shenzhen Stock Exchange may implement a delisting risk warning for Zhengbang's stock transactions.

Beijing Dabeinong had set a production target of 10 million tonnes of feed production last year. The company also acquired a portion of Hunan Jiuding's feed equity. In 2022, as prices of raw materials for feed were expected to rise sharply (with the price of pigs dropping significantly), Dabeinong was anticipated to lose ¥511 million in the first half of 2022.

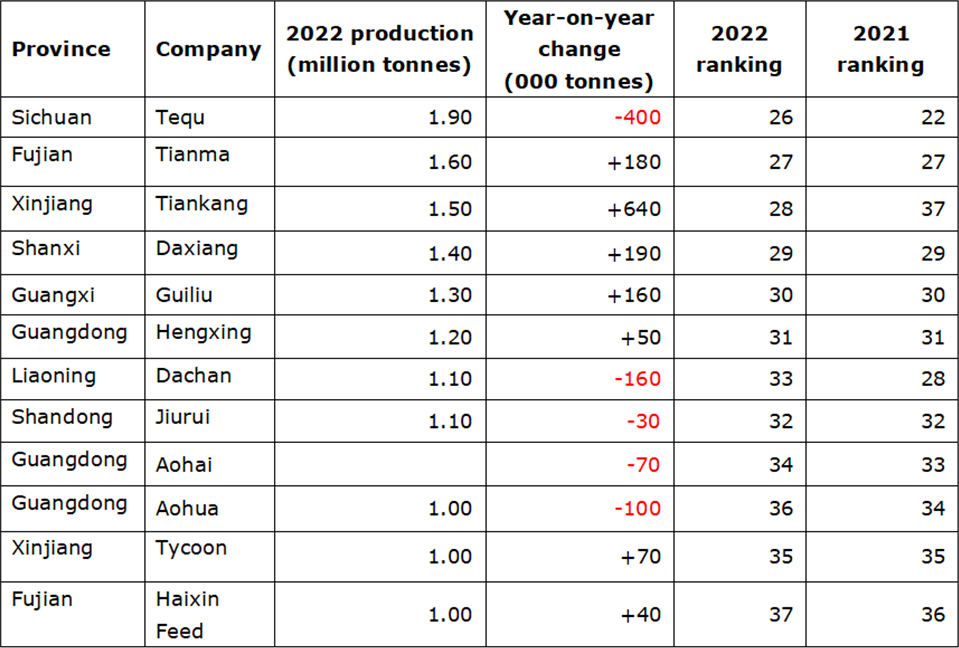

Mega-sized enterprises with a feed output of between one million and five million tonnes saw little change. In 2022, only Taikun (Xinjiang) joined the million-tonne group.

The output of several other groups, which were close to a million tonnes, was unable to make a breakthrough. The feed output of Dacheng and Jiurui suffered a drop, and this was attributed to the reduced production of pig feed.

Enterprises that had more than one million tonnes of feed output in 2022 faced several factors, including:

- The enterprises had seen growth slowed down significantly, and the growth rate of their feed production is the same as that of China's total feed production. The gradual closing down of feed mills, the slow Chinese economy and weak consumption have affected China's animal husbandry. Feed consumption in China is on a decline, affecting the further expansion of large groups;

- A feed enterprise with an output of 5-10 million tonnes had difficulty entering the ranks of those with an output of more than 10 million tonnes; it is also challenging for an enterprise with an output of fewer than one million tonnes to break past one million tonnes. Intense market competition and accelerated integration have contributed to their hurdles.

As China slowly returns to a pre-COVID norm, the consumption of animal husbandry products is expected to rebound, which will then benefit both the Chinese animal husbandry sector and the feed industry.

The gradual recovery of China's hog production capacity this year will lower the price of hogs and the pressure of operating costs. In light of this development, some enterprises may experience expansion leading to increases in feed production.

Additionally, some groups, which have focused on constructions and improvements within the hog industry chain, will continue to increase the number of hogs slaughtered in 2023, thus driving an increase in feed production.

This year, the consumption of broiler chickens and laying poultry is expected to drive a rise in poultry feed production; as such many enterprises will be increasing their production.

- David Lin and Shi Tao, eFeedLink