April 8, 2026

Thailand Livestock Operating Signal Q2 2026

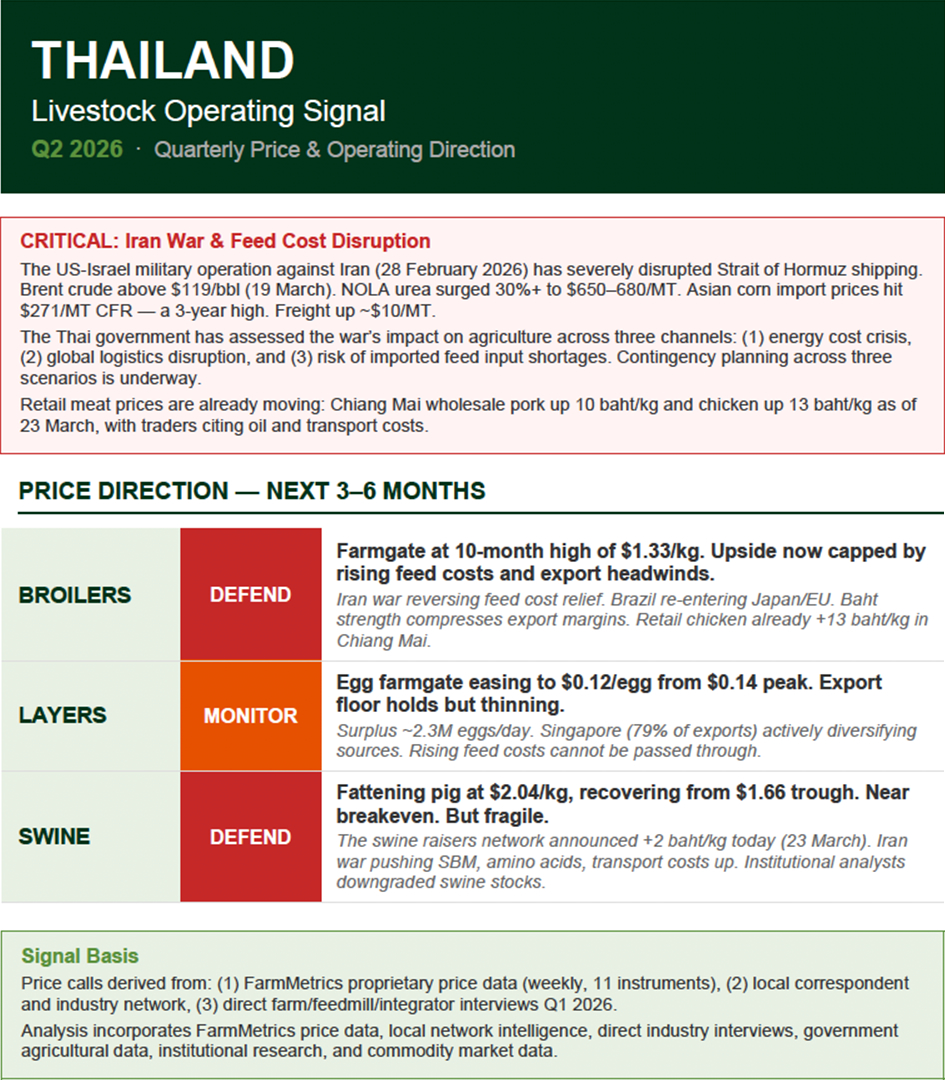

BROILERS — DEFEND

Feed cost relief was the main margin driver — now reversing.

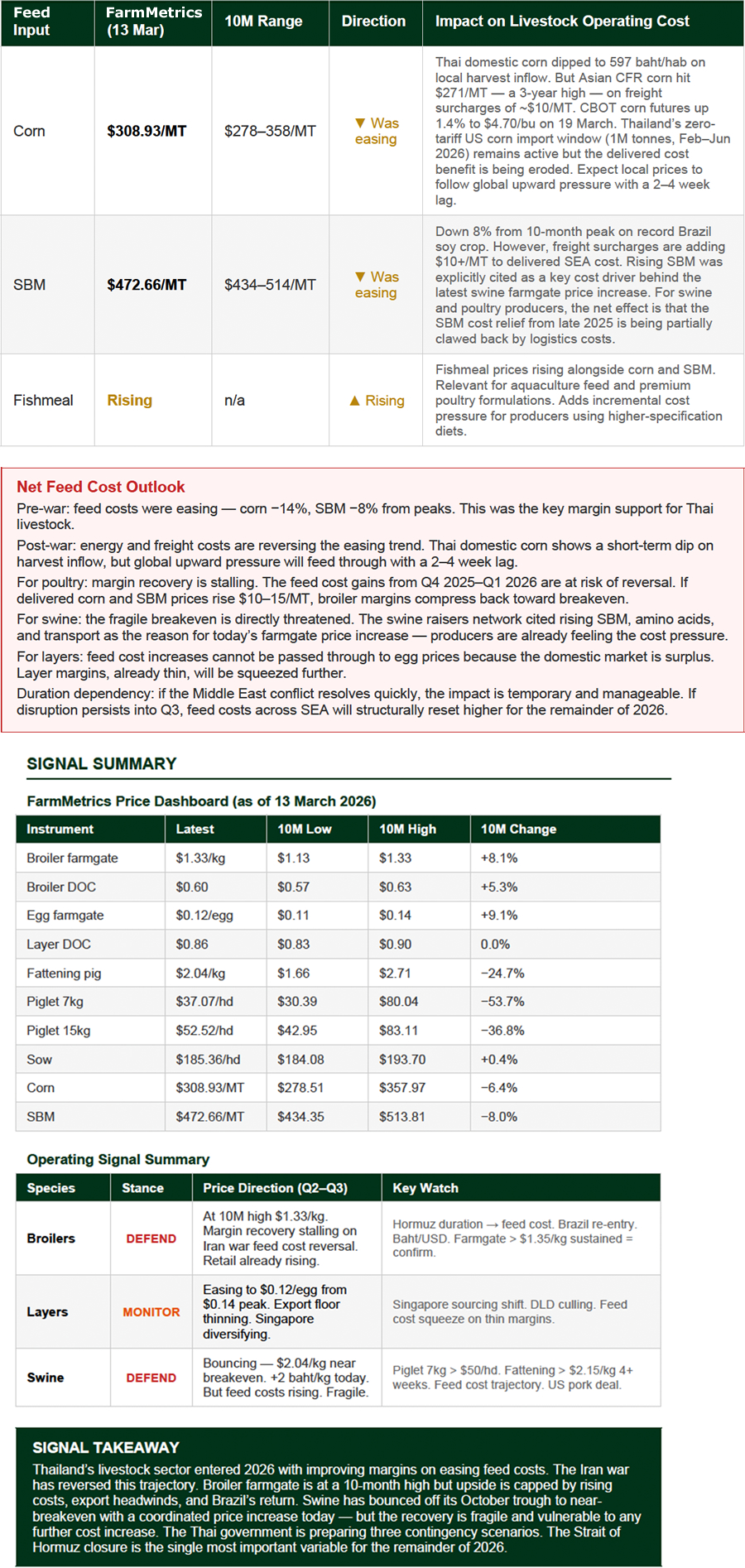

Corn eased from $358/MT (July 2025) to $309/MT (March 13) — a 14% decline. SBM down from $514 to $473/MT (−8%). This created the best feed cost environment since early 2023. However, the Iran war has pushed Asian corn import prices to $271/MT CFR (a 3-year high) with freight up ~$10/MT. Thai domestic feed corn dipped slightly to ฿597/hab (US$16.58) last week as local harvest enters market, but global upward pressure from Brent above $119/bbl and CBOT corn futures (+1.4% to $4.70/bushel on March 19) will feed through with a 2–4 week lag. The zero-tariff US corn import window (1M tonnes, Feb–Jun 2026) remains active but its benefit is being eroded by shipping costs.

Export growth is slowing and headwinds building. Industry projections show 2026 chicken production at 3.47M tonnes (+0.9%, slowing from 1.3% in 2025). Processed chicken export growth forecast at 3.2% (from 5%), chilled/frozen at 2.4% (from 5%). Brazil regained HPAI-free status October 2025 and is re-entering Japan and EU — Thailand’s two markets accounting for 60%+ of export value. Chinese processed chicken is ~14% cheaper than Thai product in overlapping markets. Baht strengthened 5.8% against USD in late 2025. Global logistics disruption and rising freight are additional headwinds for agricultural exports.

Domestic demand constrained but retail prices rising. Industry expectations are that farm prices flat in 2026 despite easing feed costs, because rising management/utility costs and government retail price controls limit pass-through. However, the Iran war is now pushing retail prices up: Chiang Mai chicken retail rose from ฿75/kg (US$2.08) to ฿88/kg (US$2.44) (+฿13/kg / US$0.36) on March 23, with traders citing oil and transport. Our feed mill interviews indicate domestic order books flat to slightly down.

Integrator placement discipline holds. DOC price stable at $0.60/chick (range $0.57–0.63 over 10 months) confirms steady but non-expansionary activity. Institutional analyst views on chicken remain positive on easing feed costs and improving export margins — but these assessments predate the Iran war's full feed cost impact.

Prolonged Hormuz closure pushes feed costs higher, compressing broiler margins back toward breakeven despite the nominal farmgate high. Brazil re-entry into Japan/EU and baht strength cap export upside. Farmgate sustained above $1.35/kg for 4+ weeks with stable feed costs would confirm recovery — neither condition is currently met.

--------------------------------------------------------------------------------

Egg farmgate easing to $0.12/egg (13 March), down from $0.14 peak in September 2025. Price stability depends entirely on the coordinated export mechanism. Without it, the domestic surplus overwhelms the market.

Domestic surplus is structural at ~2.3M eggs/day. Thailand produces ~43.4M eggs daily. The DLD and 16 major producers coordinate exports to manage surplus — the "PS SUPPORT" initiative targeted 60M surplus eggs for export by December 2025, lifting farmgate from ฿3.00/egg (US$0.08) to ฿3.40/egg (US$0.09). Jan–Sep 2025 exports: 388.63M fresh eggs (+27.3% YoY). Singapore takes 79%, Hong Kong 9%, Japan 7%.

Singapore concentration is the structural fragility — and Singapore is diversifying. Thailand holds only 19% of Singapore's egg import value; Malaysia dominates at 64%. Singapore has approved 11 source countries including Indonesia as a new supplier. Any shift in Singapore's sourcing directly pressures the Thai export price floor.

Retail margin pressure squeezing SMEs. The Central Small-Scale Egg Producers Trade Association has formally complained to the Department of Internal Trade that major supermarkets are running promotions below farmgate. Mandatory GAP certification adds cost for mid-size farms. Layer DOC at $0.86/chick is flat over 10 months — restocking not aggressive but not declining.

DLD 2026 breeding stock import plan risks deepening surplus. The plan could add up to 1.89M layer chicks annually. Without strict culling protocols, the structural surplus worsens.

Rising feed costs from the Iran crisis add margin pressure that cannot be passed through. The export-administered egg price is a ceiling as much as a floor. Layer producers absorb any cost increase directly.

Singapore sourcing diversification. DLD import quota without matching culling. Egg farmgate falling to $0.11 signals the export mechanism losing effectiveness. Rising feed costs on already-thin margins.

--------------------------------------------------------------------------------

Fattening pig farmgate at $2.04/kg (March 13), recovering from $1.66/kg trough in October 2025. Near breakeven but fragile. Q1 2026 production cost at ฿65.57–68.60/kg (US$1.82–1.91) per industry data. The swine raisers network announced a further +฿2/kg (US$0.06) increase effective March 23, pushing Bangkok reference to ฿70–72/kg (US$1.94–2.00).

The bounce is driven by supply management, not demand recovery. The industry implemented a "suckling pig" supply reduction scheme — 300,000 roasted suckling pigs over 6 months (~50,000/month) to cut piglet supply entering the fattening pipeline. Production was 21.7M head in 2024 (+6.2% YoY); 2025 expected to decline 1.63% on government Pig Board measures to reduce sow numbers; 2026 expected +0.25%. Medium-scale farms have reduced sow numbers 40–50% after sustained losses. In early February, farmgate was ฿58–60/kg (US$1.61–1.67) with losses of ฿300–800 per pig (US$8.33–22.22).

Piglet prices still signal weak restocking intent. 7kg piglet at $37.07/head (13 March) — down 54% from $80 a year ago. Has bounced from $30.39 low (late February) but remains far below levels that indicate genuine commercial restocking. 15kg piglet at $52.52/head, down 37% over 10 months. Sow price flat at $185/head — no speculative breeding activity.

Iran war is now pushing costs back up — the razor-thin margin is at risk. Industry sources confirm rising SBM, amino acid, transport, and oil prices as the reason for today's price increase. SBM has eased from $514 to $473/MT, but freight surcharges and energy costs are adding back. Institutional analysts have downgraded major Thai swine-exposed stocks, citing worsening outlook. If feed costs rise by even $10–15/MT, the margin at current farmgate levels disappears.

Retail pork prices rising fast. Chiang Mai wholesale pork jumped from ฿89/kg (US$2.47) to ฿99/kg (US$2.75) on 23 March (+฿10/kg overnight / US$0.28); retail from ฿170/kg (US$4.72) to ฿180/kg (US$5.00). National retail pork prices up ฿5–15/kg (US$0.14–0.42) in March depending on cut. This price pass-through supports farmgate recovery but risks demand destruction if consumers switch to chicken.

Malaysia pork export opening but tiny; US pork import risk unresolved. Malaysia approved chilled/frozen Thai pork imports from 4 facilities — expected value THB 4B but only ~2% of total production. The US-Thailand trade framework (October 2025) includes US pressure for duty-free pork access; Thailand has agreed to a small quota (<1% of domestic consumption) as a "test the market" phase with ractopamine-free requirement. Thai producers and the opposition People's Party are pushing back.

Piglet 7kg sustained above $50/head and fattening pig sustained above $2.15/kg (~฿74/kg / US$2.06) for 4+ weeks would confirm genuine recovery. Current prices are moving in the right direction but feed cost trajectory is adverse. The critical question: can farmgate price increases outpace rising input costs?

--------------------------------------------------------------------------------

Feed costs were easing through Q4 2025 into Q1 2026 — this was the single most important margin support for Thai livestock operators. The Middle East conflict has disrupted this trend. Rising energy costs, freight surcharges, and supply chain uncertainty are now feeding through to delivered feed input prices across the region.

This report is produced by EFL AG-DATA for professional subscribers to the FarmMetrics INSIGHT service. All price data sourced from the FarmMetrics database unless otherwise attributed. Secondary sources cited inline. This report does not constitute investment or trading advice. Reproduction or redistribution without written consent is prohibited.

Next issue: Q3 2026 (July 2026)

Please read more at:

https://farmmetrics.eflagdata.com/global/market-forecast-and-analysis

EFL AG-DATA, a Singapore-based startup, has developed FarmMetrics INSIGHT -- a market data platform delivering real-time insights on feed additives, macro ingredients, and livestock markets across China and Southeast Asia.

Interested in exploring the full features and data? Start a free trial by signing up here: https://farmmetrics.eflagdata.com/global/sign-up . Or reach out to us at inquiry@eflagdata.com.

- EFL AG-DATA