March 27, 2015

Brazilian chicken's dangerous dependence on foreign oil

A promising 2014 turns into a sour new year as fluctuating energy markets cut demand from leading importers.

By Eric J. BROOKS

An eFeedLink Hot Topic

Six months ago, it was thought that Russia's ban of European and American chicken would briefly boost Brazil's broiler export growth close to levels last seen at the turn of the decade. This however, was not to be.

Six months ago, it was thought that Russia's ban of European and American chicken would briefly boost Brazil's broiler export growth close to levels last seen at the turn of the decade. This however, was not to be. Caught between improving competitiveness and deteriorating market conditions, Brazil's broiler sector is having a mixed year. On one hand, UN FAO price data shows that compared to the first quarter of 2013, the last two years has seen Brazil's live broiler prices fell less than 10% while feed costs dropped by approximately 35%.

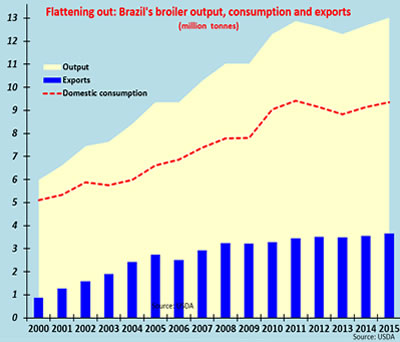

These improving profit margins stimulated output to higher than anticipated levels. From 12.678 million tonnes, the USDA was forced to revive its 2014 Brazilian broiler meat output estimate to 12.692 million tonnes. That is a 3.1% increase is a new record high and follows feed cost driven production declines of 1.7% and 2.7% in 2012 and 2013 respectively.

The domestic market also did well, with its consumption rise being revised from 2.8% to 3.5%, and totaling 9.137 million tonnes, approximately 55,000 tonnes more than anticipated.

Supply rises, aggregate demand falls

Unfortunately, this increases in supply and higher domestic demand is being more than offset by a drop in late year exports which curtailed the 3.60 million tonnes originally forecast down to 3.56 million tonnes. With exports increasing by 2.2% and output by 3.1%, a 42,000 cut in the export forecast was counterbalanced by a 54,000 tonne upward revision in domestic consumption.

Going forward however, the 2015 export forecast has been slashed by 160,000 tonnes, from the originally anticipated 3.825 million tonnes to 3.665 million, but domestic consumption is only running 58,000 tonnes ahead of expectations, making for an emerging oversupply situation. Oddest of all, this export drop off occurred even though from August 2014 through to March of this year, Brazil's real fall 28% against the currency of its world poultry market's greatest competitor, the US dollar.

It was not supposed to turn out this way. In the third quarter of last year, Russia's ban of US and EU poultry imports was supposed to create an export bonanza for Brazilian chicken -and at first, it did.

From a mere 47,292 tonnes in 2013, Brazilian broiler meat shipments to Russia nearly tripled, totaling 124, 939 tonnes. With Russia making no secret of its intention of substituting Latin American chicken in place of American and European imports, many forecasted Brazilian chicken meat exports could total 4 million tonnes this year. Striking several US states but not Brazil, even bird flu was on the side of higher Brazilian broiler meat exports at one point.

Oil, Thailand, Turkey cause export losses

Unfortunately, an unexpected crash in world oil prices disrupted the anticipated export surge. Five years ago, before Thai chicken started re-taking its pre-bird flu share of the EU frozen poultry meat market, this would not have been the case. However, the years since 2012's lifting of Thai chicken's ban from the EU has seen Brazil redirect a large portion of its broiler meat exports from Europe to the Middle East and North Africa, and more recently, Russia.

As a result, by mid-2014, nearly 40% of Brazil's poultry meat exports were being purchased by either Middle Easter OPEC countries or petroleum exporting Russia. When the price of oil plunged by more than 50%, so did the foreign exchange revenue of oil exporters from Saudi Arabia to Russia -and with it, their monetary capacity to import Brazilian chicken.

Consequently, after enjoying a windfall from Russia's substitution of Brazilian chicken in place of European and American imports, the year ended with a sharp drop off in exports. For example, Saudi Arabia, which bought 18.5% of all Brazilian chicken exports in 2013, unexpectedly cut its import volume 6%, from 688,884 tonnes in 2013 to 647,718 tonnes last year. Kuwait slashed its Brazilian broiler meat exports an even steeper 10.7%, from 113,624 tonnes to 101,627.

Only Middle Eastern states that depended on natural gas exports (whose price did not fall as much) or financial services such as Qatar or Oman bucked the trend. Even so, their combined export increases amounted to less than 10,000 tonnes; and were completely swamped by export losses in other parts of the Arab world.

Even Russia, which appeared on track to import over 150,000 tonnes of Brazilian chicken, bought 25,000 tonnes less than this amount, when the crashing ruble made it unable to continue procuring mass meat imports late last year. Instead of buying 200,000 to 300,000 tonnes of chicken, Brazil would now be lucky if Russia buys the roughly 125,000 tonnes it did last year.

In January for example, exports ran 80% above what they were in the same month of 2014 (before Russia banned US and EU chicken) -but 15% below December's volume. That implies that unless Russia economic situation miraculously improves, its demand for Brazilian chicken is at best levelling out.

Moreover, intensified foreign competition made the late year export drop-off all the worse. With its transport cost advantage, neighbouring Turkey's chicken made its way into Iran and Iraq. With Iraq rapidly substituting Turkish supplies, Brazil's exports to that country fell 19%, from 2013's 75,694 tonnes to 61,300 tonnes last year. Iran's imports, though far less, fell a sharper 59%, as it imported a mere 5,271 tonnes of Brazilian broiler meat, far less than the nearly 13,000 tonnes it bought in 2013.

Where oil's price did not matter, the continuing re-entry of Thai chicken into the European Union caused Brazilian chicken exports to the EU fall by 7.9% and for a third consecutive year to 226,103 tonnes. This is down from 245,486 tonnes a year earlier and over 300,000 tonnes just several years ago.

Against the oil-crash driven export drop off, East Asia provided a bright counterbalance. Despite its relatively slack poultry consumption, China's banning of US chicken caused its imports from Brazil to jump 19.6%, from 190,322 tonnes in 2013 to 227,548 tonnes in 2014. Moreover, with China expected to announce the approval of more Brazilian poultry processing plants for export some time during the second quarter, there is potential for volumes to boost shipments by more than expected in the second half of this year.

Similarly, with the real falling against the Japanese yen far more than the Thailand's baht did, despite Thai frozen chicken's re-entry into Japan after a nine year ban, Brazil was able to keep a larger than expected share of this large poultry market. Indeed, despite the Japanese market's maturity, Brazil's broiler meat shipments to this country rose 6.2%, from 389,697 to 413,879 tonnes.

Nevertheless, with losses in the Middle East, Europe and (late in the year) Russia offsetting most of East Asia's gains, 2014's exports, which the USDA projected to increase by at least 3.4%, rose a more nominal 2.2%, less than the 3.5% output gain. With the oil price drop clouding the forecast, this year's exports, originally pegged at 3.825 million tonnes and a 7.5% on-year increase, has been marked down to 3.665 million tonnes and a 3.0% increase.

But even this figure could be too high, and not just because the oil price crash is forcing everyone from the Middle East to Russia to eat less meat: For example, after Venezuela increased 2014 Brazil broiler meat imports by 24.6%, from 162,000 to over 202,000 tonnes, the petroleum price crash caused its importers to default on their payments to Brazilian exporters.

That sets up a situation where, unless this situation is settled, exports to Venezuela could fall by 150,000 tonnes or more. Hence, even with all other parts of this year's forecast staying constant, Venezuela alone could cause exports to go negative and fall below 2014 levels.

It is all a far cry from the days Brazilian chicken exports rose by 10% annually, or even the 5% pace seen in the late 2000s and turn of the decade.

Going forward, long after the oil price crash's impact stops rattling Middle Eastern demand for its chicken, Brazil finds itself trapped.

On one hand, a decelerating world poultry demand and the emergence of everyone from Thailand to Turkey makes it more difficult to keep the large market share it has. On the other hand, its 39% of world broiler exports is too large for rapid growth at the expense of competitors, who (with the exception of America) have much smaller market shares to offer. Hence, it increasingly looks like Brazil, much like America, will have to be content with output and export growth of 2% to 3% annually.

All rights reserved. No part of the report may be reproduced without permission from eFeedLink.